submitted by jwithrow.

Author: joegalt

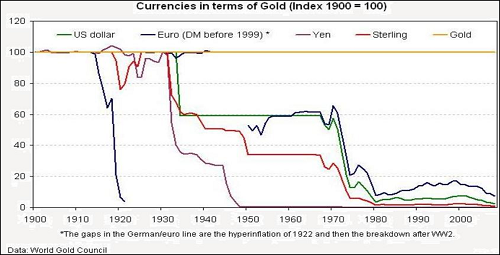

Sound Money

submitted by jwithrow.

The most important facet of free market capitalism is sound money. If you don’t have sound money then you don’t have free market capitalism – you have something else.

Sound money is simply money that serves as a reliable store of value. Put another way, sound money is money that does not constantly lose its purchasing power. Sound money affords one a reasonable expectation that one unit of money today will buy the same amount of goods and services as one unit of money tomorrow. And next month. And ten years from now.

What a novel concept!

Anyone who has taken a finance course is familiar with the time value of money principle. In finance class, we learn to discount our money over time based on the inflation rate. We are taught, correctly, that present dollars are worth more than future dollars.

What we are not taught is that this is a deformation of free market capitalism!

The general market has chosen gold and silver to serve as money throughout most of history because the precious metals are particularly well suited for this purpose: they are limited in supply, they have functional utility outside of the monetary system, and, unlike our money today, they cannot be created from nothing.

Make no mistake about it, that’s where our money comes from today: nothing. It is created from nothing and then loaned into existence at interest. See the Hidden Secrets of Money video series for a more thorough examination of our money.

You see, money should not be a function of government nor should it be a function of a central bank behind closed doors. And it certainly shouldn’t be created from nothing. This is why the U.S. Constitution only authorizes gold and silver as legal tender; the Founders knew well the virtues of sound money and the dangers of fiat currency.

Did you know that the U.S. dollar was defined by the Coinage Act of 1792 to be 371.25 grains of fine silver? This act set the standard weight and measure of the dollar in terms of silver and individuals in the market were still free to accept or reject coins of differing weights and measures as they saw fit.

But we digress.

Here is why sound money is important to you:

Every dollar to your name is constantly losing value and there is no way for you to predict how much value your savings will lose over time.

This is a direct result of the monetary system that is in place whereby central banks create money from nothing and then lend that money to governments and to commercial banks at interest. That money then enters the economy when governments spend it and when commercial banks lend it out to customers. This is done constantly and it is why your money constantly loses value. Such a system has a profound impact on people from every walk of life.

How can we accurately plan for anything long-term if our money is constantly losing value? We can only guess.

What we do know from history is that sound money leads to a stable economy while fiat money leads to booms and busts.

The general market prefers the former while big government prefers the latter.

For more information on the sound money principle see the article links below. For a lot more information on sound money and monetary history see the book links below.

An Introduction to Sound Money

The Case for Gold and Silver Bullion

submitted by jwithrow.

While gold and silver prices have declined in 2013, the fundamental case for owning gold and silver bullion is still growing.

The mainstream media has been quick to pronounce the death of the precious metals as an asset class with their evidence being the recent price depreciation of both gold and silver. Theirs is a very short term and self-serving view; the long term fundamentals have not changed.

The Federal Reserve did taper its money printing, but guess what? The creature from Jekyll Island is still creating $75 billion new dollars every single month to purchase U.S. Treasury bonds and mortgage backed securities. Meanwhile, Congress has quietly done away with the sequester spending ‘cuts’ and will continue to spend gargantuan amounts of money in 2014 – money they do not have.

What’s so humorous about this is the fact that the sequester did not cut any real spending in the first place – it simply curtailed proposed future spending increases. We suppose the thought of curtailed spending increases kept the Congress critters up too late at night.

And it’s not just the U.S.

Japan has promised to continue to keep their central bank money printer on turbo gear. Estimates suggest that the U.S. and Japan together will create nearly $2 trillion over the next 12 month period. Meanwhile, the Eurozone experiment is still on the verge of blowing up and not one single G-20 country operates with a balanced budget.

Simply put, the economies of the developed world have run up massive amounts of debt that cannot possibly be paid back in full. The massive debt has been serviced primarily by central bank funny money up to this point, but we are quite sure that the funny money policies cannot possibly last forever. And the longer the printing presses continue to run, the less valuable our paper currencies will be.

That’s why we adamantly believe that gold and silver bullion will be a vital part of a diversified portfolio in the coming years as the economic endgame of central bank funny money policy plays out.

Now, we don’t think it would be prudent to hold 100% of one’s assets in gold and silver. We look at the precious metals more as insurance against destructive monetary policies. Oh, and we should probably clarify that we mean physical gold and silver bullion in your possession, not an ETF.

So if you expect the value of your paper currency to increase then you may not be interested in holding gold or silver bullion. But if you expect the value of your paper currency to decrease then purchasing gold and silver bullion may be very wise. Given the long term fundamentals, we would suggest that the value of our paper currency is ultimately only going to go in one direction.

And that direction is back to paper currency’s inherent value…

The Lesson From Monopoly

submitted by jwithrow.

Chances are you have played the once popular board game Monopoly. In the event that you have never played the game then I would highly recommend it to you as there is a valuable lesson to be learned. And it is a classic!

The object of the game is to buy up as much real estate as possible so you can earn rental income when another player ‘lands’ on your real estate. Once you have acquired the real estate then you can invest in houses and hotels to increase your rental income.

Common thinking suggests that the game is called Monopoly because players attempt to achieve a real estate monopoly.

I do not think this is accurate, however. I would suggest that the title is derived from the fact that the ‘bank’ holds a monopoly on the money supply.

The object of the game is not to hoard the Monopoly money but rather to convert the money into productive assets. These productive assets then generate additional money in the form of rental income which can be used to subsequently purchase more productive assets when the opportunity arises.

Interestingly, the money generated from productive assets can also be used to pay taxes when the player is unfortunate enough to ‘land’ on those spots.

Players of the game understand that the Monopoly money holds no inherent value. The Monopoly money is only the accepted means of exchange with which productive assets can be purchased.

This is the lesson that we would be wise to learn and apply.

The Monopoly money is not terribly different from our fiat currency today. Our currency holds no inherent value and the central bank (Federal Reserve) holds a monopoly on the money supply. In fact, the Monopoly money may actually be better in context than our dollar because the Monopoly money maintains its value over the course of the game whereas our dollar is constantly losing value due to inflation.

So in this regard, the key to our own personal financial success is not terribly different from the object of Monopoly. The path to true wealth in life is the same as it is in the game – use the monopoly money to purchase income-generating assets. Obviously this is more complex in real life as there are a myriad of assets of varying quality to choose from and the process of acquiring these assets is much more complicated than ‘landing’ on their spot. But the concept remains the same.

Mainstream personal finance does a poor job of emphasizing this. Personal finance gurus almost exclusively suggest that we invest all of our surplus money in stocks and bonds employing a “buy, hold, and pray” strategy. This may be due to the fact that financial advisors make their living by selling the securities they tout. And while there may be a place in our investment portfolio for paper securities, they certainly do not take the place of real productive assets and one would be wise to understand the nature of the markets and the business cycle before jumping in.

Keep this concept well in mind as you build and execute your own personal financial plan. The goal is not to end up with the most money at the end of the day; it is to use money to acquire productive assets that will then provide income streams. It is essential to also employ an asset allocation model so that you are diversified across several different asset classes.

Always remember that money is just an illusion. Its only purpose is to serve as a medium of exchange and a temporary store of value. It is wise to keep a healthy amount of cash on hand at all times for both opportunities and emergencies, but any cash above your allocation would best serve you in other asset classes.

**Want more information on how to implement the lesson from Monopoly and build a sustainable asset allocation model? Are you ready to turbo-charge your retirement portfolio? Do you yearn to exit the rat-race? Is financial freedom calling to your spirit?

Do not take a backseat when it comes to your own finances. Learn everything you need to know to master your finances in 30 days by enrolling in Finance for Freedom today!

Money is an Illusion

submitted by jwithrow.

Currently we use fiat currency as money… But it’s just an illusion.

If you doubt this then ask yourself the question: What is money?

Yes, you know what money does – it buys things. But what is it?

Is it a green piece of paper with numbers and words and some symbols printed on it? Is it a card with your name, a string of numbers, and a bank logo on it?

Or is that just a piece of paper and a piece of plastic?

Fiat money is not wealth. That runs contrary to everything our society has told us, but it is the truth.

Fiat money is simply a medium of exchange which can then be used to acquire wealth… But the money itself is nothing more than a tool.

Historically, we have used gold and silver, and notes backed by gold and silver as money.

Our fiat currencies today serve the same purpose as gold and silver money… But there is one major difference. Fiat currencies can be created arbitrarily from nothing. And the central banks of the world create their fiat currencies out of thin air in massive numbers.

That’s the biggest secret of the 1% – fiat money is an illusion that is available in abundance.

While fiat money can be created out of thin air, the value of existing money necessarily falls as new money enters the economy. That’s just basic supply and demand economics. All things equal, value goes down as supply goes up.

Basically, the new money steals value from the old money. The old money can buy less and less over time. It loses purchasing power.

And that means they poach value from your bank account every time they pump a little more money into the system.

As a result, our cost of living rises over time.

Because of that, the key to financial success is not to hoard money. It’s to use money to acquire assets… Assets that rise in value over time because of all the new money being created from nothing.

The truth is, money is little more than an idea. It is an illusion… And it is only valuable as long as it is perceived to be valuable.

So if you think of money as an idea and not as a tangible asset, you will see that it takes nothing but an idea to obtain more money. But that money must then be exchanged for assets in order for it to be converted into wealth.

P.S. My Finance for Freedom course series pulls back the curtain on how money and finance really work. And it covers expert financial strategies to increase income, build wealth, and shatter the glass ceiling forever. Learn more at newly revamped https://financeforfreedomcourse.com/.

Nominal Income vs. Real Income

submitted by jwithrow.

Most of us understand that inflation is a given in our world today… But not too many of us think about how inflation affects our income.

We tend to think of our income in nominal terms rather than in real terms because that’s what we can see. We can see the numbers. After all, nominal income is our income defined only by its dollar amount.

While this just seems like common sense, it’s not the real story. You can expose the flaw of nominal income when you compare it over periods of time.

Think about this. What if our income goes from $48,000 last year to $50,000 this year? That’s a 4% raise. Not too bad, right?

Well, let’s look at our income in real terms. Real income is income defined by its purchasing power. It is nominal income adjusted for inflation.

What if inflation rises to 4% this year?

Well, the means our $50,000 salary this year will have basically the same purchasing power as our $48,000 salary last year. In other words, we didn’t get ahead. Our raise wasn’t actually raise. That’s because our income did not go up in real terms… even though our paychecks were bigger.

That’s why it’s so important to see income in terms of purchasing power… Not in terms of nominal dollars.

The real story is that the American middle class has been stuck on a giant hamster wheel for decades now. Their paychecks keep getting bigger… But their purchasing power is destroyed by inflation. They are stuck.

This is why the Austrian School of Economics views inflation as an insidious tax. If nominal income kept pace with inflation then it would not be so bad. But wages have struggled to keep up with inflation since the early 70s.

Now, wages have done a decent job of keeping up with the Consumer Price Index (CPI). But this index has been adjusted several times to ignore food and fuel price increases. They fudge the numbers to make the CPI look better.

By the way, Social Security promises cost of living increases tied to the CPI… Retirees are getting a raw deal there.

This concept also exposes the retirement folly pushed by the financial services industry.

Have you seen those commercials about your “magic number”? They say you need a certain amount of dollars saved up for retirement to live securely off the income.

But if you think in terms of real income and purchasing power… It is impossible to pinpoint a magic number. Inflation will constantly eat into it. That’s why their magic number is just a carrot on a string.

So, the only way to truly take control of your own financial destiny is to think in real terms… And to recognize the nominal view of money for the illusion that it is.

P.S. Our Finance for Freedom course series pulls back the curtain on how money and finance really work. And it covers expert financial strategies to increase income, build wealth, and shatter the glass ceiling forever. Learn more at newly revamped https://financeforfreedomcourse.com/.

Real Estate for the Long Haul

submitted by jwithrow.

Did you know that the average real estate mortgage is in existence for less than seven years?

Wall Street does and that is why they are willing to purchase and package thirty year fixed rate mortgages into securities for retail. Which is why banks are willing to originate thirty year fixed rate mortgages to sell to Fannie Mae and Freddie Mac to then sell to Wall Street to package into securities to then sell to their “muppet” clients (ask Goldman Sachs).

This is also why mortgage contracts are front-loaded with interest. You see, fixing an interest rate for thirty years (or fifteen) would be a losing position for the bank if it had to keep the mortgage on its books for the contractual length of time. Fortunately, most people are not terribly disciplined so they either refinance or sell their home within seven years of purchase.

Let’s examine this process from a financial point of view. The bank collects a myriad of origination fees when real estate is purchased and it collects an un-proportional amount of interest in the early years of the mortgage contract. Then, within seven years, the homeowner either refinances or sells the home. When the homeowner re-finances, the bank collects a myriad of origination fees once again. When the homeowner sells the home, the bank also collects a myriad of origination fees again.

Now we don’t mean to vilify bank fees, We are simply pointing out that this revolving process results in a constant drain of private capital. Each time origination fees are paid that is a little bit of capital being drawn into the banking system that could have been used by the individual to build wealth instead. Once in the banking system, exponential debt will be pyramided on top of that small amount of capital.

The point is this:

We have been buying the same real estate over and over again for decades and we have been giving up small chunks of capital each and every time the same houses have been purchased.

Wouldn’t it make a lot more sense if we just bought our homes, paid off the mortgage, and then kept them within our control? Imagine the possibilities! Of course this wouldn’t make sense in every case, but the idea is worth considering…

Shopping for a Mortgage

submitted by jwithrow.

A stable housing situation is a vital part of a self-sufficient financial plan. While home-ownership is not something that should be rushed into, we would suggest that it is advantageous to purchase a home and begin to pay down the principal balance once you are settled into a community and intend to stick around for an extended period of time. Owning a home will involve repair expenses that could be avoided by renting, but the opportunity to one day be free of a monthly housing payment is probably worth the cost of periodic home repairs.

In order to purchase a home, most of us need to obtain mortgage financing. There are a number of different mortgage types available for consumers, but a fixed rate conventional loan is by far the best option for someone who is buying a home with the intent to occupy it for the foreseeable future. As such, this article will be geared towards someone who intends to buy a home for the long haul. While the ‘long haul’ time frame is dependent upon the perspective of the home buyer, please see our thoughts on the matter here.

Unlike the other options, a conventional mortgage will allow you the choice to either escrow your homeowners insurance and property taxes as part of the monthly payment or to pay your homeowners insurance and property taxes separately. A conventional loan will also allow you to avoid private mortgage insurance (PMI) if you are able to pay 20% down up front. PMI is simply insurance that covers the lender in case the borrower defaults and it is paid by the borrower as part of the monthly payment. When obtaining a mortgage, avoiding PMI should be a top priority as it is nothing more than wasted money from the borrower’s perspective.

If at all possible, you should plan to pay 20% down when purchasing a home to avoid PMI and lock in the best terms. Some lenders will allow borrowers to also pay 10% down up front in exchange for a reduced PMI payment. If you are unable to pay 20% down initially but feel like you have the opportunity to get a great deal on a home purchase then most lenders will release the PMI requirement once you have paid the mortgage down to 80% loan-to-value (LTV) – be sure to ask about this up front. The loan-to-value ratio is simply how much you owe on your mortgage as a percentage of the home’s appraised value.

When shopping for a mortgage it can be difficult to directly compare mortgage quotes from different lenders as each lender structures closing costs differently. One lender may offer a slightly better rate but charge higher closing costs up front while another may offer a higher rate in exchange for lower closing costs. You can also choose to pay more up front to reduce the rate or vice versa when originating a mortgage. It is advisable to have a conservative idea as to how quickly you intend to pay the mortgage off before shopping for one. This way you can analyze how much you will be paying in interest and fees over the life of the loan so that you can determine which option would make the most financial sense for you.

When shopping around for a mortgage, we would recommend contacting several different lenders and asking them for an initial quote listing the interest rate and estimated closing costs. Advise them that you are shopping for a mortgage and that you will get back to them if their offer is the best. The interest rate will change every day so you will need to get the quotes on the same day that you intend to lock in an offer. Do not feel like you need to rush into a commitment, however, as you can always ask a lender to send you another quote at a later date if you are not ready to move forward initially.

Once you have several quotes in front of you, calculate the amount of interest paid over the period of time in which you intend to have the mortgage for each offer. Next, add the total interest paid to the estimated closing costs for each quote to determine the total cost of financing over the life of the loan. Whichever lender comes out with the lowest cost of financing is probably your best deal but keep in mind that each lender may estimate title insurance and attorney fees differently and that these costs will depend on the title company or attorney used for closing. It may even make sense to exclude the title insurance costs and attorney fees from your analysis if you intend to use your own title insurance company or attorney rather than the lender’s.

Mainstream mortgage advice suggests that you should lock in the lowest monthly payment possible over a thirty year period but this is not always the best way to go. Mainstream advice assumes that you will only make minimum payments and that you have no interest in paying the loan off early. We would suggest that it should absolutely be your intention to pay the mortgage off early as the idea is to minimize the amount of interest paid over the life of the loan. If you are confident that your income is stable then it may make more sense to go with a fifteen year mortgage in order to secure a better rate in exchange for a higher monthly payment. Also, be sure to play around with amortization calculators online to see how much interest you can save by paying extra on the mortgage each month.

Once you are a homeowner, be careful not to get caught up in the temptation to use your house like a piggy bank as was common during the housing bubble of the 2000’s. People love to talk about building equity in their home but this is a false premise. The term equity refers to the difference between what you owe on the mortgage and what the appraised value of the home is. Mainstream finance suggests that this equity is an asset. We suggest that it is an illusion (ever heard of anyone getting their ‘equity’ after the mortgage has been paid off?). Only the market can determine what the true value of your home is. If you do not have a buyer lined up to buy your home then you do not know exactly what your home is worth. A lender would be quick to issue a home equity loan based on the illusion of equity but this would only serve to increase the amount of interest you are paying each month.

Rather than thinking in terms of building equity, we think that it is far more wise to focus on paying off the mortgage as quickly as possible without sacrificing other opportunities. Just imagine the extra cash flow that would be available to you if you no longer had to make a mortgage payment.

Eliminating your monthly housing expense will greatly increase your resiliency and self-sufficiency and that should be your ultimate goal when shopping for a mortgage in our humble opinion.

Steps to Self-Sufficiency

submitted by jwithrow.

This list is certainly not comprehensive but it is our hope that it serves as food for thought.

1. Become money-conscious

Before you can begin to create self-sufficiency and build wealth, you must become money-conscious. Wealth does not come to those who are careless or lazy and it does not come overnight with a stroke of luck. You must begin to recognize that nearly everything that you do has an impact on your self-sufficiency and accumulation of wealth. You must begin to recognize the rules of the universe as it relates to money. And you must begin to take action immediately. Begin to track your expenses tirelessly and eliminate unnecessary spending where possible. This does not require you to become “cheap” but it does require frugality. Once you become money-conscious you will identify ways to reduce your expenses and you will free up additional income to use towards the attainment of self-sufficiency.

2. Consider contributing to a 401(k) if your employer matches your contribution

After assessing your income and expenses and getting your financial house in order, consider contributing to a 401(k) up to the employer match percentage each month. It is important to review the vesting requirements (time of employment required before you can cash out the matching contributions) and determine whether or not you will be at this company for that length of time before deciding to contribute to the plan. The employer match will serve to multiply your deferred savings and your 401(k) contribution will reduce your taxable income. We would not recommend contributing any more than the employer match rate as 401(k) plans are very limited and the rest of your income would better serve you elsewhere. Be aware of the fact that you will have to pay a 10% penalty to the IRS if you cash out the 401(k) prior to retirement but the tax shelter provided will serve to offset some of this penalty. With that said, we would suggest that a 401(k) plan is not a very strong part of a retirement plan and that the funds accumulated would probably better serve you as capital to be deployed once you have developed a more specific investment plan. The 401(k) will allow you to automatically put aside a very small amount of income for use once you are farther along on your road to financial freedom. This vehicle may not be suitable for everyone, but it may be useful if you are still working on creating a sound investment or business plan.

3. Develop a plan to eliminate all consumer debt

You must eliminate all consumer debt before you can effectively begin to build wealth and your first target should be credit card debt. The interest rate on your credit card, in all likelihood, will far outweigh any return on investment that you could consistently generate with your money. So develop a plan to pay all credit card debt off as soon as possible. The most effective way to do this is to determine exactly what dollar amount you can afford to pay towards your credit card debt with each paycheck, and to pay that amount immediately as soon as your paycheck is received. Do not leave yourself short on other bills but make sure that you are paying a sizeable chunk of debt down each month at the same time. If you have multiple credit cards then you should pay the card with the highest interest rate off first. Once all credit card debt is eliminated, move on to the next highest interest rate obligation that you have. The one exception to paying down the highest interest rate debt first is if you have a smaller obligation that could be paid off very quickly in order to free up additional cash flow that could then be directed towards the higher interest debt. While eliminating consumer debt may seem like a long and slow process, be patient and persistent. Imagine a world in which you have no consumer debt to pay and imagine how much extra money you will have at your disposal once you are free of consumer debt.

4. Develop a plan to eliminate or reduce mortgage debt

This step could possibly be interchanged with the next steps depending on your situation but the idea is to either eliminate or reduce your monthly mortgage debt significantly now that you have additional free cash flow from eliminating consumer debt. While the many possibilities cannot be described in this article due to the variety and complexity of mortgage types, we do discuss mortgages in more detail here. Broadly speaking, assess your mortgage and determine if an action can be taken to enhance your financial situation (reducing the LTV, refinancing, etc).

5. Build a six month cash reserve

If you have not already built a cash reserve then now is the time to do so (if you have dependents then you may want to consider making this step two). A cash reserve should be extremely liquid so that you have access to the money in a timely manner in case of emergency. A standard checking account would serve this purpose. Interest bearing savings or money market accounts are acceptable choices although you can rest assured that the interest paid on these accounts will be negligible. Cash under the pillow is another option. Gold or silver bullion could be a wise choice but you will probably want to have direct and immediate access to some cash. While six months is a good benchmark, you could consider building a one year cash reserve as well. Just make sure that you are prepared to sustain yourself and meet obligations in case of an emergency.

6. Set up an IBC whole life insurance policy

If you are unfamiliar with the IBC (Infinite Banking Concept) strategy then this step will require some research before you are comfortable with the idea. Now, do not be put off by seeing this recommendation for ‘life insurance’ – learning about an IBC policy will completely shatter your preconceived notions about what life insurance can do. The reason you have not heard about this type of policy before is because Wall Street would go out of business very quickly if the masses learned and implemented this financial strategy. An IBC policy is about building an ever-growing pool of capital in a way that is advantageous in both the tax and liability realms. The IBC strategy is not about death benefits and it is not about rates of return – these are just bonuses.

When structured properly, IBC policies allow you to funnel income into the policy rather than a bank account. Unlike your bank account, your life insurance cash value is secure from creditors, bail-ins, and bank runs. The cash value also generates a small rate of return without sacrificing liquidity – you can access your cash value tax free at any time for any reason. The implementation of this strategy does require a long-term commitment because it will take on average 8-10 years before an IBC policy ‘breaks even’ internally (cash value equals premium outlay).

Please feel free to email us if you would like more information on this concept.

7. Build diversified income streams in fields that interest you

At this point you have done your due diligence and are in a financial position that will allow you to work on pursuing income in ways that are enjoyable to you. If you are already engaged in work that is satisfying and meaningful to you then this step may not be relevant to you. But if you are like most of us who simply tolerate or maybe despise our job then now is the time to make changes. And even if you are content in your current profession it may be wise to build side businesses as economic conditions are tentative at best at this juncture in time.

Start by deciding what it is that you would like to do with your time and then develop a plan to generate income from your chosen field. While this is an embarrassingly simplistic statement, it is entirely possible to generate income from any good or service for which there is a market. Build a big business. Build several small businesses. Buy rental properties. Become a freelancer in your areas of expertise. Whatever your plan is, the important thing is to engage in work that is enjoyable and meaningful to you – income is useless if it comes with the sacrifice of happiness.

8. Convert income into real assets

Once you have developed a source or sources of stable income then it is time to convert this income into real assets. The most widely accepted choices would be gold and silver bullion, real estate, and/or farm land but you are not limited to these. Real assets could also be things that increase your household’s self sustainability such as alternative energy sources or a family garden. You could also choose more speculative items such as art work or a wine collection but these assets would be much less liquid and thus much more risky (well, the wine would be liquid but in a different kind of way). If you venture into the realm of these speculative investments then make sure that you have a portfolio consisting of the more widely accepted assets as well.

Conclusion:

Note that we wittingly omitted any mention of investing in paper equities (stocks, mutual funds, exchange-traded funds, bonds). The first reason for this is that the financial services industry has sold this type of investment as the only one suitable for retirement which is a lie. There may be a place for this type of investment within your portfolio but it will require much diligence and should serve only as one asset class amongst several within your portfolio. Holding a mixture of stocks across different industries is said by the experts to be the key to diversifying your portfolio. We would suggest that holding a mixture of stocks, real estate, gold and silver bullion, etc. would be the key to a diversified portfolio and that holding only paper equities would be terribly risky. So if you do choose to include equity investments in your portfolio please make sure that you do your research and that you also diversify amongst other, more tangible asset classes as well.

Think of real assets as a ‘backing’ to the cash value of your IBC whole life insurance policy that we discussed in step 6. By building a significant pool of capital (IBC policy) and solidifying it with real assets you are doing exactly what the elite central banks do – except without resorting to fraud. The central banks, Wall Street, and the power elite in general have done a wonderful job of convincing the masses that the key to success is to accumulate exclusively stocks and bonds. And this is true. But what they did not disclose to the masses is that such a strategy is key to the success of the central banks, Wall Street, and the power elite, not the masses themselves.

We hope that this brief article serves as a guide towards maximizing your personal liberty, resiliency, and self-sufficiency.

Always remember that happiness, fulfillment, and calmness of mind and spirit are the most precious of commodities and be mindful not to lose sight of these ideals on the road to building wealth and obtaining self-sufficiency. Also, never be afraid to follow your heart and stand on your principles; this life is but a journey in search of experience and wisdom, and that journey is best undertaken to the beat of one’s own drum.

Ozymandias

submitted by jwithrow.

“I met a traveller from an antique land

Who said: “Two vast and trunkless legs of stone

Stand in the desert. Near them on the sand,

Half sunk, a shattered visage lies, whose frown

And wrinkled lip and sneer of cold command

Tell that its sculptor well those passions read

Which yet survive, stamped on these lifeless things,

The hand that mocked them and the heart that fed.

And on the pedestal these words appear:

`My name is Ozymandias, King of Kings:

Look on my works, ye mighty, and despair!’

Nothing beside remains. Round the decay

Of that colossal wreck, boundless and bare,

The lone and level sands stretch far away”.

– Percy Bysshe Shelley